The Real Cost of Big DAC

Two emerging challenges to direct air capture showcase the systems nature of climate-solving, and it's exhausting

It’s become clear over the last few years that we won’t be able to head off the worst effects of climate change with emissions reduction alone; we need to remove the carbon dioxide that’s already out there, and we need to do it at scale.

Now, multiple emerging challenges threaten the future of the most theoretically scalable carbon removal method we know of to date: direct air capture and storage.

Given my own involvement with the Carbon Business Council, a nonprofit trade association representing over a hundred carbon removal organizations including direct air capture companies, and my other work and commentary in the broader carbon removal space, this story was a difficult one to broach. But we climate and carbon people are the ones that need to be taking the hardest look at our own assumptions around solutions if we’re going to be successful in selling them to the world, so here goes.

The first challenge: we probably won’t see $100 per ton DAC

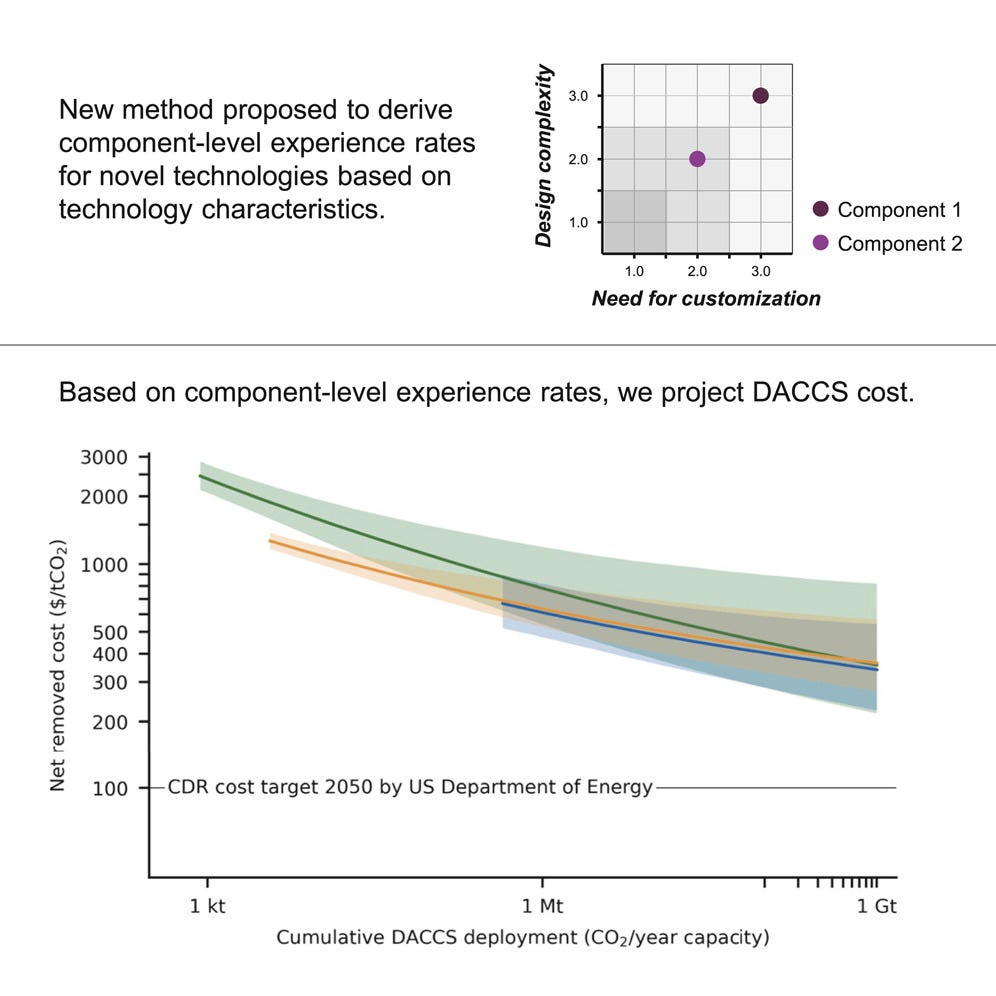

A new research report now estimates a much higher than previously assumed projected cost for direct air capture carbon removal combined with storage. Instead of the Holy Grail of sub-$100 per ton that’s commonly cited as a future price target, this report says that net costs will be in the range of $226 to up to $835 per ton, with median costs around $360 per ton at a scale of 1 gigaton removed per year. This analysis was conducted by researchers at ETH Zurich – the highly regarded Swiss public research university known for its engineering, science & technology programs, in collaboration with the Institute for Science, Technology and Policy, a federally funded research and development center in the US.

There are 3 important things I want to highlight about this study:

1— Unlike much of the current commentary on carbon removal, including cost estimates, this research wasn’t performed by a buyer, seller or other stakeholder in the broader world of carbon money.

Instead, it was carried out by the head of ETH Zurich's Energy and Technology Policy group, who’s also director of the Institute of Science, Technology and Policy and an elected member of the Swiss Academy of Engineering Sciences, alongside the head of ETH Zurich’s Climate Finance and Policy Group, alongside one brave graduate student.

2— The research focuses on three specific types of DAC technology associated with the three most established direct air capture companies in the world (aka the ones currently selling credits to airlines, Frontier and other blue chip buyers): Carbon Engineering, Climeworks and Heirloom.

It is incomplete in that it does not cover every type of emerging “DAC 3.0” technology. However, it’s just as important to understand the techno-economics behind the most established players since they’re the companies accruing the most purchases and generally setting the bar.

3— Although the study’s findings showed that costs for these three DAC variations will be unlikely to approach the magic $100 per ton threshold, the researchers were quick to point out (repeatedly) that DAC could still be a good alternative to sustainable aviation fuels, which are expensive, questionable in their actual sustainability, and not scalable due to land use issues. That the researchers felt it necessary to state this multiple times throughout their report shows how hard it is to run counter to an industry consensus, but it also underscores a key takeaway:

DAC doesn’t have to solve every carbon removal problem, and maybe that’s fine. Put otherwise, companies like Heirloom, Climeworks and Carbon Engineering don’t have to sell the lowest cost credits, and maybe that’s also fine.

We’ve commonly understood carbon to be a commodity. But, as the world becomes more discerning around greenwashing and hard-to-abate industries run out of better options, might we start to see a decommodification of carbon removal that supports greater price diversity?

I’m not a DAC bear

I hope and pray that direct air capture will scale, but no one’s listening to my birthday candle wishes. Instead, what has mattered to most observers is cost and its role in driving adoption of new technologies.

Technologies have taken hold either because smaller size alongside dropping costs have driven proliferation (semiconductors, iPhones), or because they served initially niche use cases that gave them a foothold to compete against the default option (semiconductors again, backhoes).

DAC’s great hope, then, is either that emerging DAC 3.0 technologies will come in and disrupt their forebears with ultra low cost, high scale approaches or that price insensitive, special needs customers or sectors will help it cross the wide chasm that’s still ahead.

There’s already evidence that both of these could happen:

Companies like Spiritus (among too many others to list here!) have taken a modular and passive / low opex approach to drive down costs and simplify potential deployment

Climeworks just announced a deal with SWISS and Lufthansa as part of those airlines’ net-zero hedge against the even more expensive — and far less reliable — landscape of sustainable aviation fuels

But, even the most pro-DAC among us have to consider a future where DAC stays expensive — or at least one where the biggest, best-known, best-funded and closest-to-scale DAC companies aren’t able to bend their cost curves as much as the world expects them to.

What the research says

The researchers’ work showed cost ranges at the 1 gigaton per year in cumulative capacity to be closer to the following:

$341 per ton for liquid solvent DAC systems like Carbon Engineering’s approach, with a range of $226–$544/tCO2 at 90% confidence

$374 per ton for solid sorbent DAC like Climeworks’ approach, with a range of $281–$579/tCO2, and

$371 per ton for calcium oxide ambient weathering DAC like Heirloom’s approach, with a range between $230–$835/tCO2

1 gigaton per year of removed carbon is an important scale threshold because it’s what the US has said it plans to remove annually.

They used a more granular methodology than is typical

Instead of asking experts for projections, or using equations borrowed from solar and battery cost curves, they derived component-level experience rates to get probabilistic cost extrapolations using multi-component experience curves.

Incumbent DAC technologies use a combination of novel and off-the-shelf components, making them a complex aggregation of different experience curves. By individually analyzing and synthesizing experience curves from multiple components that are themselves at different levels of maturity, researchers were less likely to overestimate cost reductions.

The researchers then combined these hard COGs with projections for electricity costs, including factoring in falling costs for tracking solar PV and storage, and variations for nuclear and geothermal sources of energy. Crucially, they did not factor in costs for community engagement and relations (remember Enel Energy’s $587M trespassing mistake?), which we’ll come back to shortly.

Why $100 per ton matters (and why it doesn’t)

The $100 per ton price is more than an easy-to-remember round number. It’s the price target established by Frontier, the pioneering Advanced Market Commitment coalition that includes Stripe, Alphabet, Shopify, Meta, and McKinsey, in collaboration with the US Department of Energy.

Frontier’s requirement that any technology it backs have a path to being affordable at scale is backed by a lot of research, and its purpose is to spur a global market for widespread carbon removal by using early demand commitments to help high-priced suppliers eventually derisk their technologies and bring prices down to drive mass adoption.

To its great credit, Frontier originally intended this price target to reflect an average carbon removal cost across a variety of solutions, spanning nature-based and engineered carbon removal methods. But, it has since been twisted to become the de facto benchmark for every type of carbon removal, including DAC.

$100 per ton is now commonly viewed as the price at which DAC becomes economically viable, to the point where the World Economic Forum has pointed to $100 per ton as the key price threshold and the International Energy Agency has gone so far as to say, “With deployment and innovation, capture costs could fall to under USD 100/tCO2.”

As the ultimate backstop technology – that is, a technology that can serve as a direct substitute for a limited resource like land for planting a trillion trees – direct air capture plays an incredibly important role in our ability to remove up to 12 billion tons of CO2 every year until 2050 to reach global net zero per the IPCC’s estimate, since in theory it’ll be there for us when all other methods reach their natural limits.

But if we believe that affordability is the key unlock to deployment scale, and that upfront investment is the key unlock to affordability, then we have to start asking ourselves how much it’s going to cost.

Together Climeworks, Carbon Engineering and Heirloom have raised a total of $925M* across dozens of rounds of private financing rounds. This may seem like a lot, or it may seem like a drop in the bucket to “unfuck the planet,” as Chris Sacca says.

Trillions have been made in polluting and denigrating the Earth, so it may take more capital — and more time — to unwind than what we’ve come to expect in our venture scale timeline world.

That’s Heirloom’s $53M + Climeworks $762M + Carbon Engineering’s $110M.

The second challenge: CO2 pipelines are not popular

In the last few months, a separate controversy has been brewing across multiple states in the midwest over several thousand miles of CO2 pipeline that would transport point source captured CO2 to its final resting place deep underground in North Dakota.

Carbon transport is a bigger business than you might think. One pipeline company, Summit Carbon Solutions, could be eligible for as much as $18B in federal tax benefits over the next 12 years. Even if it doesn’t hit that maximum, it would still likely generate enough in tax credits to cover all of its construction and operating costs.

Summit and other CO2 pipeline companies are facing backlash from local landowners and environmentalists who are concerned about the companies’ property seizure tactics and the threat of CO2 pipeline rupture, which has created major public health hazards in the recent past.

While these pipelines could eventually be used for direct air capture, their current most common use case is for transporting CO2 captured from ethanol facilities — not exactly the climate-friendly solution its biofuel name would suggest (land use problems + emissions at production + emissions at combustion), but nonetheless a precursor technology enabling critical DAC infrastructure.

The enemy of my enemy is my friend

Recently, in a classic Enemy of My Enemy is My Friend move, the National Corn Growers Association has teamed up with its longtime foe the American Petroleum Institution to oppose EVs and call on the federal government to ease its EV mandates and go for blended fuels instead (here’s their recent letter to President Biden).

Where Big Corn and Big Oil used to fight over who got what share of the gas tank, now they’re forming a united front against the common enemy of electrification. Of the 812 billion pounds of corn the US produces each year, 36% of it goes towards the production of 15.36 billion gallons of ethanol, most of which is consumed in American vehicles.

Because DAC and storage will likely rely on the same pipeline infrastructure and sequestration wells, this dynamic could see EVs’ success hampering direct air capture deployment at a time when we know we need both mitigation and removal.

Ugh, systems problems

So, now we start to see the systems nature of climate-solving:

Direct air capture stakeholders are struggling and will continue to struggle with cost curves, which will worsen as transport and storage infrastructure is hampered;

Pipeline builders are losing battles with landowners up and down the midwestern corridor as they build infrastructure for ethanol producers today and carbon removal companies tomorrow;

EV stakeholders who are not only up against Big Oil but now also Big Ag, and possibly the CO2 pipeline builders that stand to make billions from ethanol;

With climate change raging through the middle of it all.

Climate change is a systems problem that requires an Everything Everywhere All At Once approach (hat tip to friend and fellow climate investor Kirsti Chou for the best adaptation of a movie title to an existential problem).

As a climate human, I often wish I had a magic wand that I could use to get everyone to adopt EVs, among many other changes.

But if my wand worked, what would happen to corn farmers? And then, what would happen to CO2 pipelines? And then, what would happen to DAC prices?

Systems thinking is the opposite of having a magic wand (for example, a magic wand called technology). Instead, it forces us to look high/low, near/far and everything in between, all at the same time.

Systems problem solving may require an even harder set of tasks: moving forward with imperfect knowledge, seeking spot solutions for specific industries instead of blanket answers for all problems, and embracing mistakes as part of the natural process of revision and evolution.

I’m still pro-DAC, and I still think the world is underestimating both our incumbents and their disuptors, but make no mistake: this is one of the hardest problem we’ll ever have solved.

Great article/pod Susan !

re: $100 price:

A few years ago in there were a lot of data points where people calculated the social cost of carbon at $100 and lobbied the incoming Biden administration to adopt $100 as the government's social cost of carbon. I remember around that time people talking about the $100 target for DAC cost and it made sense to me that the social cost of carbon must be equal to the terminal DAC cost, because theoretically this is the price where it would be economically rational (and not purely catalytic) for society to purchase CDR.

I assumed it was not a coincidence when EU ETS prices rallied and were capped at 100 euros in '22 and '23.

Most recently, the EPA calculated the social cost of carbon at $190 per tonne but there doesn't seem to be any effect on how people talk about DAC/ CDR affordability or emissions trading markets.

I wonder if anyone reading has a more scientific or authoritative view on the relationship between the social cost of carbon circa 2020 and pricing targets in the various carbon trading markets / the origin of the mythical $100 CDR carbon tonne.